Query

Please provide a literature review of studies that empirically assess the impact of illicit financial flows on economic growth.

Caveat

This Helpdesk Answer surveys the literature to present original studies of the empirical relationship between IFFs and economic growth. The literature review looked for evidence on the effects of IFFs on source, transit and destination countries, but found that most of the research focuses on source countries.

The Helpdesk Answer attempts to apply some appraisal of the quality and robustness of the studies included. However, the authors note that, due to the sophisticated nature of statistical models employed in many of the studies considered, ascertaining the reliability of the methodologies used and the viability of some of the research findings reported would require a thorough examination of each study by a skilled econometrist.

Finally, this literature review tried to prioritise studies that used a ‘narrow’ conceptualisation of IFFs and capital flight that excludes what UNCTAD refers to as legal activities, such as tax avoidance and legal forms of profit shifting. However, the authors of some of the studies included did not clearly specify the exact definition of IFFs they employed when assessing the impact on economic growth.

Defining illicit financial flows

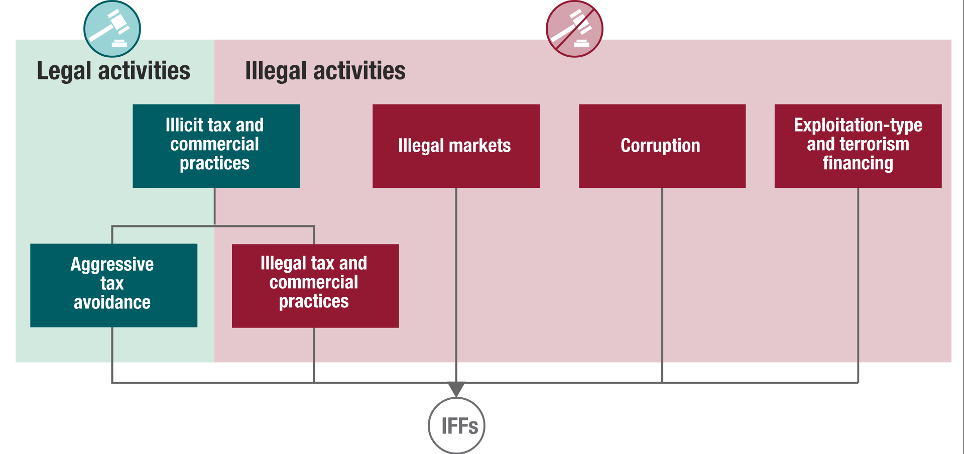

The debate on the definition of IFFs often centres on whether to adopt narrow or broad definitions. Narrow definitions focus on strictly illegal activities, such as money laundering, tax evasion, organised crime, corruption and other illegal flows. Conversely, broader definitions include activities that are technically legal, such as exploitation of regulatory loopholes and aggressive tax avoidance (U4 n.d.).

Figure 1: Activities that may generate illicit financial flows

Source: UNCTAD (no date)

Indeed, the very term ’illicit’ implies not only strictly illegal activities but could also legally questionable or ethically dubious practices that go against the ‘spirit’ but not necessarily the ‘letter’ of the law (Mehrotra and Carbonnier 2024). Further complicating this definitional issue is the shifting regulatory landscape, notably the introduction of legislation in certain countries targeting some of the methods and loopholes that have historically facilitated tax avoidance (Mehrota and Carbonnier 2024: 12).

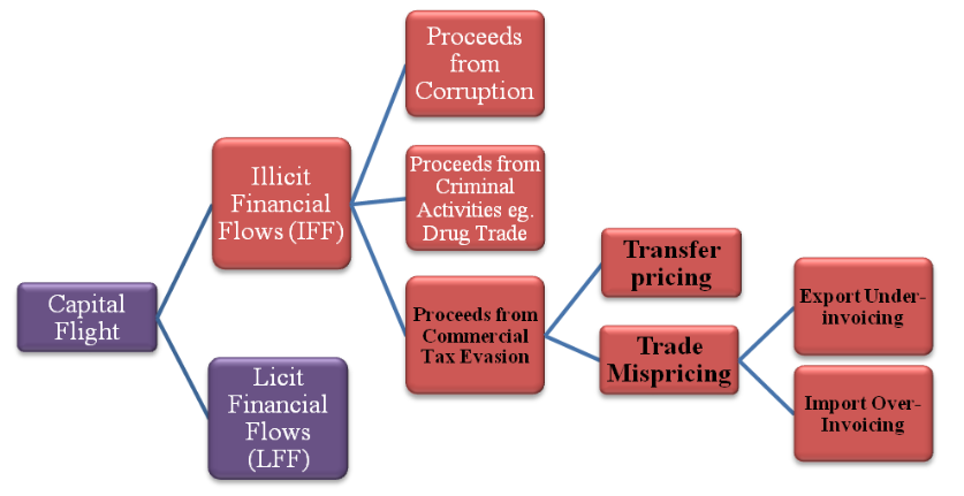

An example of a broad definition is that provided by UNCTAD and UNDOC, which construes IFFs as ‘financial flows that are illicit in origin, transfer or use, that reflect an exchange of value and that cross country borders’(U4 n.d.). Another example is the definition used by the Tax Justice Network, which states that IFFs can include ‘the concealment of the proceeds of crime or corruption; tax evasion; tax avoidance and tax planning; hiding wealth from public agencies, business associates, or family members’(Fowler 2018). In addition, some analysts use the concept of IFFs interchangeably with the term capital flight (see Box 1), a phenomenon which may be both legal and sizeable.

Figure 2: Illicit financial flows and capital flight

Source: Mevel et al. (2013: 7)

Examples of a narrower definition include that provided by Global Financial Integrity (n.d.) ‘the illegal movements of money or capital from one country to another’. The UNODC (2016) proposed a definition of IFFs as ‘all cross-border financial transfers which contravene national or international laws’. The IMF uses a similar, narrow definition that also focuses on illegality: ‘cross-border financial flows associated with illegal activities in their origin (e.g., results of illegal acts such as corruption), transfer (e.g., conduit tax arrangements), or destination (e.g., funds used for illegal purposes such as TF). This definition excludes legal tax avoidance flows’ (IMF 2023).

Any empirical analysis of the impact of IFFs on economic growth must consider the scale of IFFs, which ultimately depends on the definition being applied. For instance, including tax avoidance in the definition can naturally make the scale of IFFs, and thus any potential impact on economic growth, appear larger.

The working definition of IFFs adopted by this Helpdesk Answer is aligned closer to the narrow definition espoused by the UN and IMF, namely cross-border money flows that are illegal in either their origin, transfer or intended use. This definition does not include tax planning and (legal forms of) transfer pricing, but encompasses the following financial flows:

- Illegal tax evasion and deliberate trade misinvoicing. Such funds may be licit and legal in their origin but not in their transfer.

- Funds derived from criminal markets in illegal goods such as arms trafficking, drug trafficking, human smuggling and other forms of organised crime. These markets generate funds that are illegal in their origin.

- Illegal corrupt activities, notably bribery and embezzlement, can be an important source of IFFs.

- Financial flows related to hybrid warfare or adversarial influence operations (Bak 2021), terrorist financing, as well as the evasion of sanctions or export controls. These funds may be licit and legal in origin, but illicit in their intended use.

Generally, this Helpdesk Answer attempts to apply the narrow definition of IFFs during the literature review. However, some studies that employ broader definitions of IFFs are mentioned as they provide empirically significant results.

Box 1: Capital flight or illicit financial flows?

Reuter (2017: 3-4) observes that, while empirical research on the consequences of IFFs has been limited, the macroeconomic impact of capital flight has been subject to greater study (see the final section of this Helpdesk Answer for an overview of many of these studies). He notes, however, that the relevance of the findings of the economic effects of capital flight to research on IFFs remains unclear, and indeed there is controversy as to the nature of the relationship between IFFs and capital flight. In fact, Ndikumana and Boyce (2019:2) point out that the two terms are sometimes used interchangeably.

As in the case with the concept of IFFs, there are many competing definitions of capital flight. At its broadest, it refers simply to an outflow of money or securities (Johannesen and Pirttilä 2016: 1). Narrower definitions of capital flight as illegal – or at least unrecorded – financial (out)flows are conceptually very similar to the definitions of IFFs proposed by Global Financial Integrity and the IMF (see page 6).

For instance, Ndikumana and Boyce (2019: 2) argue that ‘all capital flight is illicit, [but] not all illicit financial flows are capital flight’. This is because, for them, capital flight refers to the illicit transfer of assets that is not reported to government authorities, whereas IFFs relate to the illicit origin, transfer or use of funds (Ndikumana and Boyce 2019: 3). In practice, this implies that illegally acquired funds moved abroad through officially recorded transfer mechanisms would not count as capital flight. As such, in their view, capital flight is a constituent element of the wider phenomenon of illicit financial flows.

As discussed below, some of the most prominent approaches used to estimate the volume of illicit financial flows adopt methods developed in the literature on capital flight, notably the sources-and-uses (residual method) and ‘hot money narrow’ estimates, which are based on balance-of-payments data (Collin 2020: 51).

Indeed, Brandt (2022: 794) observes that illicit financial (out)flows could be an important component of estimates of capital flight computed on the basis of discrepancies in balance-of-payments statistics. Because, contrary to Ndikumana and Boyce (2019), Brandt (2022) adopts a definition of capital flight that encompasses legal (recorded) transfers of capital, he therefore views illicit financial flows as a constituent element of the broader concept of capital flight. Brandt thus argues that as estimates derived using the sources-and-uses and ‘hot money narrow’ methods capture both licit and illicit cross-border movements of capital, the figures calculated are invariably larger than the true total volume of IFFs.

All this has led Reuter (2017: 24) to conclude that the concept of IFFs remains poorly defined, with little understanding of the ‘relative importance of the component sources’, which has important implications for measurement and policy.

Determinants of economic growth

To understand the economic impact of IFFs, it is necessary to first identify the main dimensions and relevant drivers of economic growth. Economic growth usually refers to an increase in a country's production of goods and services, typically measured by changes in GDP or GDP per capita.

However, the significance accorded to different variables of economic growth differs between schools of thought among economists. Many economists accord primacy to factors such as capital accumulation, labour growth and technological progress (e.g. Solow 1956). In contrast, so-called ‘institutionalists’, such as Acemoglu and Robinson (2012) stress the centrality of institutions, arguing that inclusive governance and strong rule of law promotes investment, productivity and innovation, while extractive (or corrupt) institutions hinder development. Other potentially significant variables of economic growth mentioned in the literature include the level of available human capital (as shaped by investments in healthcare, education and research) (Allen et al. 2013; Romer 1986) and structural transformation – the emergence and expansion of innovative, high productivity industries (Rodrik 2014).

Together, these perspectives underline that the determinants of economic growth are multidimensional. As such, studies of the potential impact of IFFs on growth could focus on the effects of illicit flows and a range of other variables, such as innovation, institutional quality and domestic investment.

Methods to estimate the scale of IFFs

There are several different approaches to measuring IFFs. These can focus on inferences made from publicly available macroeconomic statistics, balance-of-payments statistics, trade statistics, company level information or, alternately, leaks such as the Panama Papers, or periods of extraordinary windfall profits (Brandt 2022: 792). The choice of estimation method can have significant implications for attempts to estimate the effect of IFFs on economic growth. Indeed, Kahler et al. (2018) observe that the relative dearth of empirical research on IFFs is the result of the difficulty in calculating the scale of the phenomenon.

Macroeconomic imbalances methods

Macroeconomic approaches rely on identifying discrepancies in national financial accounts, particularly in the balance of payments. Frequently used methods to estimate IFFs via an analysis of macroeconomic balances include the so-called ‘sources-and-use’ and ‘hot money narrow’ methods.

The sources-and-uses method (also known as the residual method) was first developed by the World Bank (1985). This approach tracks discrepancies in the balance-of-payments statistics such as reported sources of funds (e.g., foreign aid, trade surpluses, foreign direct investment) and their use (e.g., capital investments, current account deficits or foreign reserve accumulation). In the balance of payments, sources of capital inflows should only exceed their uses when there are unrecorded or unexplained capital flows (i.e. naturally there should be a balance between the inflows and outflows recorded). By analysing any net changes in sources and uses, researchers can make inferences about the volume of capital flight (Collin 2020: 51; Johannesen and Pirttilä 2016: 2). Importantly, this measure of capital flight includes both legitimate and illegitimate transfers of capital.

To better differentiate between legal forms of capital flight and illicit financial outflows hidden from official statistics, researchers have developed an alternative method focused on isolating the magnitude of unrecorded capital outflows (Collin 2020: 51). The ‘hot money narrow’ method is thought to more precisely capture the magnitude of illicit flows as it measures changes in deposit banks’ foreign assets and portfolio investments (Brandt 2022: 797; Duri and Rahman 2020: 3). As mentioned, a country's balance-of-payments accounting should be in balance in terms of capital in and outflows. However, sometimes discrepancies appear in the IMF’s balance-of-payments statistics database, which are labelled as net errors and omissions (NEOs). The hot money narrow method assumes that discrepancies in NEOs are more likely to capture funds that are moved quickly and discreetly out of the country in question. Such abrupt capital movements can potentially be an indicator of illegality, rather than ‘ordinary’ capital flight (Collin 2020: 52; Brandt 2022: 797; Duri and Rahman 2020: 3).

Using the hot money narrow method, Global Financial Integrity (2019) has estimated that in 2015, approximately US$342 billion in illicit capital outflows left developing countries.

These two methods offer broad coverage and provide insights into financial imbalances at the national level. However, the common problem with approaches to measuring IFFs that focus on scrutinising balance-of-payments data, such as the hot money narrow and sources-of-use, is that they can struggle to disentangle illicit financial flows from legitimate ones (Brandt 2022: 797). For this reason, the results may overestimate the scale of IFFs. After all, not all NEOs are illicit. As discussed below, some researchers, such as Madrueno and Silberberger (2023) reduce the estimates calculated using the hot money narrow method (such as those produced by Global Financial Integrity (2017)) by up to 50% to account for potential overestimation of IFFs.

Finally, Brandt (2022: 797) also points out that neither the sources-and-uses nor the hot money narrow approach are able to capture ‘more sophisticated intra-firm approaches to transferring earnings from one country to another in order to avoid corporate taxes’.

Trade-based IFF estimation methods

Unlike the two methods discussed above, trade-based methods of estimating IFFs involve comparing exports and imports between partner countries. This seeks to capture the scale of trade misinvoicing, a common channel for IFFs, which involves manipulating trade volumes or customs invoices to evade taxes or move money illicitly. For instance, if the import value is significantly lower (accounting for shipping/freight rates as well as insurance costs)33f431503302 than the export value, it could indicate under-invoicing of exports (to evade customs duties). If the import value is significantly higher than the export value, it could suggest over-invoicing of imports (a way to smuggle money out of a country) (Collin 2020: 52).

Analysts using trade gaps analysis to estimate IFFs can use data from the IMF's Direction of Trade Statistics or the UN's COMTRADE database to compare what one country reports as exports to another country and what that country reports as imports from the first country (Collin 2020: 52; Mehrotra and Carbonnier 2024: 3; Duri and Rahman 2020: 6). For instance, if a low-income country reports a higher import value than the export value reported by a high-income trading partner, this mismatch could indicate an outflow due to potential misinvoicing. Analysts can also estimate IFFs via an analysis of discrepancies in customs documentation (Mehrotra and Carbonnier 2024: 3)

Some of the most widely cited estimates of the scale of illicit financial flows are based on combining estimates derived from balance of payments discrepancies with calculations about the scale of trade misinvoicing (see Boxes 2 and 3).

However, according to Brandt (2022: 802), IFF measurements based on trade misinvoicing data are premised on some questionable assumptions. First, they do not always account for the fact that shipping freight costs and insurance rates differ depending on commodity. Discrepancies can be quite high for landlocked countries, or for countries that trade in commodities with time-sensitive cargo, such as perishable goods. Second, variations in how countries categorise goods can create artificial discrepancies at a commodity level, complicating analysis. Third, it is often assumed that industrialised countries have accurate import reports, which is not always the case (Brandt 2022: 802-806). Fourth, poor data quality can make it difficult to determine fair transaction values, especially given the diversity of goods traded. Standard customs systems (such as HS, NAICS or SITC) do not always capture product differences, nor quality (Mehrotra and Carbonnier 2024).

Therefore, while trade misinvoicing undoubtedly provides a window into some irregular capital movement, aggregates based on trade gaps are at best an imprecise measure of IFFs (Collin 2020: 55; Mehrotra and Carbonnier 2024: 6; Brandt 2022: 802).

Box 2: Global Financial Integrity estimates

To estimate the total volume of IFFs, Global Financial Integrity (2017: 1) combines estimates of trade misinvoicing660f402a6096 with the estimated volume of unrecorded capital flight based on balance of paymentsad1019931d52 discrepancies using the hot money narrow method. GFI (2017: 1) estimates that illicit financial outflows were somewhere between US$620 and US$970 billion in 2014. A full 87% of their estimated total volume of illicit financial outflows is accounted for by trade misinvoicing, with balance of payment discrepancies (‘hot money’869eb3bfe47c) accounting for only 13% (GFI 2017: 13).

To quantify the scale of trade-based misinvoicing, GFI uses the gross excluding reversals (GER) method to calculate illicit outflows based on export under-invoicing and import over-invoicing. This examines mirrored statistics on bilateral trade between developed and developing countries, assuming that the real value of trade is closer to that reported by developed countries. Estimated shipping and insurance costs of up to 10% are deducted from discrepancies identified, to produce the estimated total of value of trade-based misinvoicing (Collin 2020: 54).

Johannesen and Pirttilä (2016: 8) point out that this approach to estimate the volume of trade-based misinvoicing has not been widely used in academic literature, which is perhaps due to the four questionable assumptions discussed by Brandt (2022: 802) above.

Box 3: Estimates by Ndikumana and Boyce

While the approach of combining residual (sources-and-uses) method and trade misinvoicing (hot money) estimates is most commonly associated with Global Financial Integrity, Boyce and Ndikumana have produced several rounds of estimates of capital flight for African countries using a similar methodology (Ndikumana and Boyce 2010; 2011; 2019; 2021; Boyce and Ndikumana 2001; 2012).

Their method involves calculating capital flight using the basic approach pioneered by the World Bank (1985) of the residual method of discrepancies between inflows and outflows of foreign exchange recorded in the balance of payments (Ndikumana and Boyce 2019: 1). However, they make numerous methodological adjustments to correct for the magnitude of external borrowing, exchange rate fluctuations, debt write-offs, inflation, unrecorded remittances (Ndikumana and Boyce 2010).

Like Global Financial Integrity, Ndikumana and Boyce (2019: 7) also recognise that ‘data on trade transactions in the BoP may be affected by erroneous or deliberate misinvoicing of the value of imports and exports’. They therefore add estimates of trade misinvoicing based on comparing bilateral trade data to arrive at their final estimate of illicit capital outflows.

Data on debt comes from the World Bank’s International Debt Statistics database while data for the other variables are taken from the balance of payments. The measurement of trade misinvoicing is based on data from the Direction of Trade Statistics (DoTS) database compiled by the IMF and the COMTRADE database published by the United Nations.

Ndikumana and Boyce have updated their methodology to compute trade misinvoicing several times, most recently in 2021. First, the 2021 methodology adjusts the computation of aggregate trade misinvoicing. In response to the lack of comprehensive reporting in some African countries on imports and exports, they scaled up discrepancies between African countries’ export and import data and the corresponding values reported by their trading partners in the group of advanced or industrialised countries (Ndikumanav and Boyce 2021: 2-3). In addition, they tweaked the method used to estimate the cost of insurance and freight, which is then subtracted from any residual difference between countries’ trade data.

While they make no claim that their estimates reflect the full extent of illicit financial flows (as opposed to the illicit/unrecorded transfer of capital abroad), the series of estimates of capital flight produced by Ndikumana and Boyce have been widely used by researchers to assess the impact of capital flight on economic growth and domestic investment on African countries (see the studies discussed in the final section of this Helpdesk Answer).

IFF estimations based on discrepancies between assets and liabilities

Another approach to measure IFFs has been to examine discrepancies between countries in terms of where assets are located vis-a-vis liabilities. In international finance, every asset (like stocks or bonds held abroad) should have a corresponding liability (the entity issuing or holding the debt). Individuals or companies hiding wealth offshore are unlikely to report their overseas assets, meaning the asset position of source countries is artificially low. On the other hand, even tax havens generally report the liabilities on their books accurately, even if they do not disclose data on beneficial owners (Brandt 2022: 798; Collin 2020: 53).

The Zucman method, named after economist Gabriel Zucman, examines mismatches between declared assets and liabilities across countries. This approach uses data from tax havens and secrecy jurisdictions as well as from global financial records, such as the IMF's Coordinated Portfolio Investment Survey and the Bank for International Settlements (BIS). Further scholars have adopted this approach in recent years, including Alstadsætter et al. (2019), who use bilateral bank deposit data to estimate the stock of wealth residing in tax havens.

The method is generally considered to be more precise than other models in measuring cumulative capital flight to tax havens (Brandt 2022: 798) and appears corroborated by the fact that estimates of unreported wealth are largest for tax havens (Collin 2020: 57). However, while wealth held offshore might indicate a risk that this wealth is of illicit origin, this is not necessarily the case (Collin 2020: 57). Moreover, like the balance-of-payments methods already mentioned, the discrepancies in aggregate data it identifies could be partly explained by measurement errors. Finally, this method is only suited to uncover financial wealth, as opposed to corporate tax avoidance or wealth held in other forms of assets such as real estate (Brandt 2022: 798) .

Phantom FDI

Yet another method entails looking into so-called phantom FDI. Damgaard et al. (2019) argue that some foreign direct investment (FDI) does not relate to genuine investments into the local economy but corresponds to so-called phantom FDI: investments that simply pass through a jurisdiction. For instance, Luxembourg receives a level of FDI similar to the United States while, at the same time, outward FDI from Luxembourg is very close to the level of FDI inflows to the country. This indicates that this FDI simply passes through Luxembourg as a transit destination and does not correspond to genuine economic activity, indicating that such phantom FDI is a technique to move money. By using data from the IMF’s Coordinated Direct Investment Survey, researchers have been able to classify different investments into real and phantom investments (Brandt 2022: 801-802). Researchers that have applied this method in their analysis have estimated that out of a US$40 trillion of total investments in 2017, US$15 trillion was not related to actual economic activity (Brandt 2022: 801-802).

Gravity modelling

So-called gravity models are used in economics to predict the volume of trade or financial flows between different countries, based on variables of how attractive one jurisdiction is to investors from another country. In other words, factors like GDP growth, physical distance and cultural affinity determine the size of the ‘gravitational pull’ of a given country on capital based in other countries.

Since the technique was first developed by Walker (1999) in relation to money laundering, other researchers have also adopted this approach, by developing an ‘attractiveness index’ of how attractive a country is for money launderers, based on factors such as GDP per capita, banking secrecy, anti-money laundering safeguards, the ratio of bank deposits to GDP, the level of corruption or the presence of armed conflict. As applied by Maloney et al. (2019: 45, 119), for instance, the gravity model estimates the volume of money laundering in a country, which equates to the ‘sum of domestic proceeds of crime that remain in the country plus the flow into the country of monies for laundering from all other countries’.

Beyond money laundering, gravity models can also be used to calculate an ‘illicit premium’ that can serve as a proxy for the scale of IFFs more generally. For instance, if Country A sends notably more investment to a country designated as a secrecy jurisdiction than would be explained by variables that typically predict investment patterns, this unexplained excess might plausibly be partly composed of illicit finance. Pérez, Brada and Drabek (2012, cited in Collin 2020: 58) analysed FDI from transition economies and found that jurisdictions labelled as ‘jurisdictions of primary concern’ by the US State Department have often received more FDI than explained by a traditional gravity model that accounts only for legal activities (Collin 2020: 58). This could be considered a potential indicator of illicit flows, though gravity model estimates do not always attempt to estimate actual volumes of IFFs. This is because it could be the case that other, unobserved variables make a particular destination attractive to inward investment.

Firm-level data

Analysing firm-level data, such as multinational corporations’ profit margins and transfer pricing could also provide insights into tax avoidance and profit shifting. For instance, one could assess the magnitude of IFFs by looking into the profitability of multinational companies versus domestic corporations. However, this approach is mostly relevant to study the scope and scale of multinational companies’ profit shifting (see Brandt 2022: 809), which is not usually illegal and may fall outside of the narrow conceptualisation of IFFs discussed above.

Other ways of estimating IFFs

As an alternative to methods that rely on macroeconomic or trade data, researchers have attempted to understand IFFs from either leaks or from the study of potentially revealing financial movements during periods of extraordinary economic circumstances (Brandt 2022: 810). For instance, some researchers have found that a 100% increase in the price of crude oil is associated with a 22% increase in the offshore bank deposits of residents of oil-rich autocratic countries, whereas there is no significant effect for residents of oil-rich countries that are not autocracies (Brandt 2022: 810). Similarly, in another study, Andersen et al. (2022) find a positive correlation between aid disbursements to highly aid-dependent countries and bank deposits from those aid-recipient countries in offshore financial centres with high levels of banking secrecy.

Summing up, the diversity of methods and data sources employed to measure IFFs reflects the complexity of capturing reliable data on this hidden phenomenon; no approach is without drawbacks. Moreover, Duri and Rahman (2020: 14) highlight that a reliance on economic datasets can lead to a view of IFFs that foregrounds tax avoidance and trade-related flows. This may mean that IFFs arising from corrupt and criminal activity are underrepresented in the (imperfect) estimates we have.d48cbf11c1d2

How IFFs could impact economic growth

There are numerous intermediate variables, or channels, through which IFFs could potentially affect economic growth in source, transit and destination countries.

Domestic revenue mobilisation and government revenue loss

A significant channel through which IFFs may impact economic growth is the effect they have on government revenue (UNCTAD 2020: 131–132). By illicitly moving funds overseas out of the reach of the tax authorities, IFFs directly reduce the funds available for public investment. For instance, in a study of West African Economic and Monetary Union countries, Thiao (2021), finds that a one standard deviation increase in IFFs reduces government revenue mobilisation by 0.85 percentage points. Reduced public revenue limits the ability to invest in growth-enhancing sectors such as education and infrastructure (Thiao 2021: 16). Similar results are reported by Asmah et al. (2020) in their study of the impact of trade misinvoicing on the volume of tax revenues in 13 African countries, which draws on estimates of trade misinvoicing produced by Ndikumana and Boyce.

UNCTAD (2020: 131-132) argues that this revenue leakage puts a constraint on the governments’ ability to finance projects in, for example, infrastructure, healthcare and education. A multivariate regression model developed by Ortega et al. (2020) demonstrates the significance of illicit financial outflows on the quality of healthcare provision in 72 countries. Likewise, O’Hare and Curtis (2014) use estimates of illicit financial outflows from Malawi produced by Global Financial Integrity to show how the foregone tax revenue would be sufficient to provide all Malawians with essential healthcare services. As such, a weakened fiscal base hampers productivity and human capital formation, with potentially long-term impacts on economic growth.

IFFs may also have the added effect of shifting the burden of taxation in a country towards the middle and lower ends of the income distribution spectrum (Coplin and Nwafor 2019). This is because the response of some governments in low-income countries to low levels of revenue collection, partly attributable to IFFs, has been to increase forms of taxation that target household consumption. This reduces the amount of disposable income people have, the spending of which could stimulate economic growth.

Moreover, significant illicit outflows can distort source countries’ balance of payments, affect asset prices and reduce foreign reserves. As such, IFFs can have deleterious effects on the fiscal position and indebtedness of source countries. Extensive capital flight might compel governments to increase external borrowing, while foreign loans can themselves ‘trigger debt-fuelled capital flight’ in which loans ‘guaranteed by the government flow immediately and directly into foreign private accounts’ (Herkenrath 2014). In addition, the shortage of domestic capital associated with illicit outflows could increase the domestic interest rate, which can make it even harder for borrowers to service external debts (UNCTAD 2020: 130). Finally, Ampah and Kiss (2019) argue that capital outflows can precipitate a depreciation of the national currency, further increasing the cost of investment and imports. Taken together, these macroeconomic effects of IFFs can produce long-term negative effects on economic growth (Ritter 2015: 21).

IFFs hinder capital formation and distort investment patterns

IFFs damage the potential for economic transformation by lowering the rate of capital accumulation and reducing private investment and productivity (Slany, Cherel-Robson and Picard 2020: 8). IFFs divert funds away from productive economic endeavours, such as investment in research and development (UNCTAD 2020: 130). Afolabi (2024), for instance, empirically demonstrates the negative effects of IFFs on domestic investment across various regions of sub-Saharan Africa, showing a clear negative relationship between IFFs and capital formation.

IFFs also influence investment patterns in transit and destination countries, with the effects often concentrated in sectors like real estate and luxury goods (Yikona et al. 2011). Investments in these sectors tend to have lower multiplier effects on economic growth than investments in more strategic economic sectors (Yikona et al. 2011: xiv).

Box 4: Evidence of the impact of cross-border corruption on economic development

Most of the studies on the impact of IFFs on economic growth do not disaggregate the documented effects by the constituent components of illicit flows, such as tax avoidance, tax evasion, criminal markets and corruption. Nonetheless, there is some research that specifically concerns the impact of transnational corruption on determinants of economic development.

Habiyaremye and Raymond (2013), for instance, find that corrupt practices on the part of foreign firms are associated with local firms in host countries spending less on research and development, reducing their ability to launch and upgrade products. Interestingly, they conclude that transnational corruption involving foreign firms has a more significant negative effect on local firm innovation than petty corruption perpetrated by domestic companies. Moreover, the effect of cross-border corruption on the competitiveness and ability of local firms to innovate appears particularly pronounced in low and middle-income countries (Habiyaremye and Raymond 2013).

The impact on economic development of the enforcement of measures intended to curb cross-border corruption have also been studied. Christensen et al. (2024) examine the impact of the US Foreign Corrupt Practices Act (FCPA) on economic development in African regions with significant natural resource endowments. The authors study the effects of the increase in FCPA enforcement since the mid-2000s on proxies for economic development (cash-wage employment and nighttime light emissions) in rural areas in the proximity of extraction facilities. They find that both nighttime luminosity and cash-wage employment increased in localities near extraction facilities managed by entities subject to the FCPA, relative to areas located near facilities managed by entities whose owners are not subject to the FCPA. This increase in economic development is attributed to FCPA-liable firms engaging in practices more beneficial to local communities (Christensen et al. 2024). For instance, according to the authors, FCPA regulation incentivised multinational firms to create stronger local links, such as choosing suppliers on the basis of efficiency rather than political connections, which reportedly enhanced the positive economic impact on surrounding communities.

IFFs as an enabler and cause of corruption

IFFs are closely linked to corruption (Eriksson 2018:

- Corruption facilitates many of the illegal activities that generate illicit funds.

- Corruption is itself a source of funds for IFFs.

- Corruption facilitates illegal transfers by incentivising oversight officials such as customs agents to turn a blind eye.

- Corruption facilitates the illegal use of funds once IFFs have crossed borders.

- Corruption hollows out institutions that prevent or detect IFFs (such as financial intelligence units).

The last point echoes a central theme in the literature, namely that corruption damages institutional quality, particularly in IFF source countries. Acemoglu and Robinson (2012), for instance, contend that corruption weakens the rule of law, creating an environment where rent-seeking behaviour flourishes at the expense of productive economic activity. In their view, this significantly hampers economic growth by distorting market incentives. This perspective is shared by multiple researchers who find that, while weak institutions magnify the negative effects of IFFs on productivity (UNCTAD 2020: 133), strong institutions limit the negative effect of IFFs on the economy (Padil et al. 2022: 1391; Madrueno and Silberberger 2023: 26; Afolabi 2024: 1429).

In addition, the criminal activities underlying IFFs can be significant enough to have macroeconomic effects, such as where grand corruption and rampant embezzlement leads to the gross misallocation of public resources, or where organised crime deepens the informality of the economy and distorts markets (IMF 2023).

Security and fragility

IFFs contribute to state fragility (generally in low-income countries or those affected by the resource curse) by exacerbating governance challenges and fuelling illicit economies. Cobham (2016) argues that IFFs undermine state legitimacy, capacity and the political will that that is necessary to build resilient and stable state structures. In his view, IFFs drive two separate vicious cycles: one perpetuating insecurity as illicit flows finance conflict and erode state legitimacy, and another eroding state capacity to provide the conditions needed for sustainable peace (Cobham 2016). These create feedback loops that discourage investment and stifle economic growth (Jenkins 2024: 9-10).

IFFs also have implications for national security in destination countries. IFFs facilitate the financing of organised crime, terrorism and hybrid warfare (Bak 2021), all of which may have spillover effects on economic growth.

Synthesis of evidence of IFFs on economic growth

IFFs are increasingly recognised as having profound and often detrimental effects on economic growth, particularly in developing economies where IFFs typically originate. There is a growing literature on the empirical effect of IFFs on economic performance, most of which relies on estimates by Global Financial Integrity or Ndikumana and Boyce to model the relationship of illicit outflows on GDP growth and domestic investment.

The headline findings of some of these studies are summarised below, while the methods employed in each study – and some of their potential shortcomings – are discussed in more detail in the final section of this Helpdesk Answer.

Empirical evidence on the economic impact of IFFs on source countries

At the global level, Madrueno and Silberberger (2023) find that illicit outflows have a significant negative direct relationship with economic growth and that a 10% increase in the volume of net outbound IFFs is statistically correlated with a 1.5% decline in the growth rate of gross national income (GNI) per capita (Madrueno and Silberberger 2023: 21).

Padil et al. (2022) investigate the effect of IFFs as well as the quality of governance on economic growth, focusing on nine ASEAN countries. They find that, controlling for the quality of governance, IFFs have a statistically significant negative impact on economic growth (Padil et al. 2022: 1391). At the same time, the quality of governance moderates the relationship between IFFs and economic growth.

Ndikumana (2014: 118) researched the impact of financial outflows on economic growth in Africa, concluding that, had these funds not been moved abroad, the 39 countries studied could have added an average of 2.4% to their annual GDP growth between 1970 and 2010.

In addition to the effects documented at the regional or global level, studies of the effects of IFFs on individual economies (particularly in Africa) likewise suggest that IFFs have a negative effect on economic growth. In a case study of Ethiopia, Narea (2018: 14) finds that a 1% increase in IFFs corresponds to a 2.79% decrease in the rate of GDP growth. Econometric analysis of Nigeria by Ogbonnaya and Ogechuckwu (2017)finds that IFFs and sudden capital movements can help explain more than half of the changes in the country’s economic growth (Ogbonnaya & Ogechuckwu 2017: 25-27). Similarly, research on the economic impact of trade misinvoicing in the oil and timber sectors in Cameroon estimates that, if the finances lost to capital flight and trade misinvoicing in these industries had instead been productively invested in the country, annual GDP growth could have been 0.21% higher in the 17 years between 1995 and 2001, and 0.54% higher in the period between 2002-2012 (Mpenya et al. 2015: 1).

Overall, the literature reviewed for this Helpdesk Answer and discussed in greater detail below points to three main findings. First, there is strong consensus among academics that illicit financial outflows have significant negative effects on domestic investment, particularly private investment. Second, studies that have applied so-called financing gap models, such as the incremental capital output ratio (ICOR), to estimate the potential opportunity cost of illicit financial outflows conclude that these lost funds could have contributed significantly to higher economic growth in IFF source countries (Almounsor 2017; Fisseha 2022; Mpenya et al. 2015; Ndikumana 2014). Finally, the effects of IFFs on economic growth are more significant in the long run than in the short term, pointing to the negative cumulative effect of illicit financial outflows over time (Kasongo 2022: 1; Effiom et al. 2020: 358).

Empirical evidence on the economic impact of IFFs on destination countries

There is a smaller and more limited evidence base on the economic impact of IFFs on destination countries. However, there is some indication that illicit financial inflows are unlikely to make substantial contributions to economic growth in destination countries in the long term, yet bring with them a range of economic and regulatory challenges.

The IMF (2023: 11) states that inflows of IFFs to destination countries can create inflationary pressures and market distortion. The risk might be especially acute in sectors like banking and real estate that are targeted by those looking to integrate illicit funds into the formal economy. The IMF (2023: 11) suggests, for instance, that the banking industry may encounter bubbles and reputational risks when scandals related to inbound illicit finance come to light, which could entail risks to economic stability.

Property markets may be negatively affected by inbound illicit funds. In a study of money laundering’s impact on real estate prices in British Columbia in Canada, Maloney et al. (2019: 2) find that money laundering has inflated real estate prices by as much as 5%. Similarly, looking at the laundering of proceeds from organised crime in Italy, Novaro et al. (2022: 672) find that money laundering has a statistically significant inflationary effect on house prices, except for areas in which acts of violent crime frequently occur. Transparency International UK (2017: 4) has estimated that property in London worth £4.2 billion had been purchased with suspicious wealth.

Summaries of selected studies examining the impact of IFFs and capital flight on economic growth

Note that while the analysis above draws on studies that explicitly state they empirically assess the relationship of illicit financial flowson economic development, some of the studies included below instead consider the economic impact of capital flight. See Box 1 for a discussion of the conceptual distinction.

Afolabi, J. 2024. Does illicit financial flows crowd-out domestic investment? Evidence from sub-Saharan Africa economic regions. International Journal of Financial Economics, 29(2), pp. 1417–1431.

This study investigates the impact of illicit financial outflows on domestic investment – a widely acknowledged determinant of economic growth – across four economic regions of sub-Saharan Africa (EAC, CEMAC, SADC & ECOWAS). To model this relationship for 34 sub-Saharan African countries between 2008 and 2020, the author uses data on outbound IFFs from Global Financial Integrity (GFI) and data on gross fixed capital formation from the World Development Indicators (Afolabi 2024: 1423).

Given the preponderance of trade misinvoicing in GFI’s estimates (see discussion of GFI methodology on page 11 above) this means that Afolabi (2024) is largely assessing the effects of trade misinvoicing – as opposed to other constituent components of IFFs – on domestic investment. This caveat likewise applies to the other studies discussed below that model the impact of IFFs on determinants of economic growth using GFI estimates.

To understand both the short-term and long-term effects of IFFs on capital formation, and how the relationship between illicit outflows and investment evolves over time, the study applies two regressions (panel auto regressive distributed lag and pool mean group). The study controls for variables such as GDP growth rate, money supply and institutional quality.

Afolabi (2024) finds that IFFs have a crowding-out effect on domestic investment. Both in the short and long term, and across all four economic regions under study, illicit outflows hinder domestic gross fixed capital formation (Afolabi 2024: 1429). While Afolabi (2024: 1428-29) interprets the results as ‘overwhelming evidence’ that illicit financial flows have a ‘devasting impact’ and cause ‘catastrophic effects’ on domestic investment in all four regions, the size of the effect, while statistically significant, appears relatively small. Particularly in the long term, Afolabi’s (2024: 1429) results appear to indicate that institutional quality (as measured by the World Bank’s Worldwide Governance Indicators) matters more for gross fixed capital formation than the volume of illicit outflows. This suggests that stronger institutions can play a significant role in mitigating the negative effects of IFFs.

Almounsor, A. H. 2017. New analysis of capital flight from Saudi Arabia: The relation with long-term economic performance. Applied Economics and Finance, 4(6), 17-26

Almounsor (2017) studies the impact of illicit capital outflows from Saudi Arabia on economic performance in the period 1971 to 2015. The author uses data on capital inflows, current account balances, changes in reserves from the World Development Indicators dataset, trade data from the Saudi Arabian monetary authority and the World Trade Integrated Solutions dataset.

First, Almounsor (2017) adopts the residual methodology to estimate the scale of illicit capital outflows, by considering only unrecorded outflows. To adjust for potential trade misinvoicing in balance of payment data, the author compares import and export data from the Saudi authorities with that produced by the country’s industrialised trading partners. This assumes that data from industrialised countries is more accurate, and discrepancies between those figures and the data published by the Saudi Arabian monetary authority is accounted for by trade misinvoicing. Adjustments for inflation are also made, resulting in an estimate that illicit capital outflows between 1971 and 2015 were approximately US$212 billion in 2010 prices.

Next the author employs the financing gap model developed by Nkurunziza (2014) to quantify the effect of capital flight in terms of lost economic growth. Using the incremental capital output ratio (ICOR) – which represents the amount of capital required to obtain an additional unit increase of production output – Almounsor (2017) estimates that the opportunity cost of the US$212 billion equated to 3.57% decline in economic growth, from a potential average GDP growth of 8.4% to the actual GDP growth between 1971 and 2015 of 4.8%.

Chirowamhangu, E. 2023. The effect of illicit financial flows on Zimbabwe’s economic growth and development.

Chirowamhangu (2023) examined the effect of IFFs and capital flight on Zimbabwe’s economic growth and development in the period 1980-2020.

For data on illicit financial flows, the author uses data on trade misinvoicing published by Ndikumana and Boyce (2021). Data on GDP and the various control variables (such as trade openness, FDI, inflation and government consumption expenditure) was taken chiefly from the World Bank (Chirowamhangu: 2023: 57).

The author then applied an auto regressive distributed lag regression model to analyse the data, which indicated that trade misinvoicing had a statistically significant negative coefficient relationship with GDP in the long run; each unit increase in capital flight equated to a reduction in GDP by 0.02%.

Combes, J. L., et al. 2019. Assessing the effects of combating illicit financial flows on domestic tax revenue mobilization in developing countries. Etudes et Documents, No 7, CERDI.

Combes et al. (2019) study the effect of illicit financial outflows on domestic tax revenue mobilisation in 67 developing countries between 2004 and 2013. Data on tax revenue is taken from the International Centre for Tax and Development’s Government Revenue Dataset and the IMF’s tax revenue dataset. Data on total (as opposed to net) illicit outflows comes from Global Financial Integrity’s estimates, which combine the World Bank’s residual method and trade misinvoicing estimates based on IMF data.

The authors then use a ‘propensity score matching technique’ to analyse whether countries that comply with FATF Recommendations have higher domestic tax revenues than non-compliant countries. This is found to be the case; improving compliance with FATF Recommendations – used as a proxy for curbing IFFs – is thought to equate to a 1.2% increase in domestic revenue mobilisation as a percentage of GDP.

Effiom, L., et al. 2020. Capital flight and domestic investment in Nigeria: Evidence from ARDL methodology. International Journal of Financial Research. 11(1).

Effiom et al. (2020) study the empirical impact of capital flight from Nigeria on domestic investment over the period of 1980–2017. The authors adopt the residual approach to computing the volume of capital flight developed by the World Bank (1985) and use data from the World Development Indicators to do so. Data on domestic investment, interest rates, exchange rates, inflation rates, total debt, and real gross domestic product data were sourced from the Central Bank of Nigeria Statistical Bulletin 2018.

Effiom et al. (2020) use the auto regressive distributed lag (ARDL) econometric methodology to estimate the coefficients between the variables of interest. The study found a significant and negative relationship between capital flight and domestic investment in Nigeria. The long-term impact of capital flight on domestic investment was found to be larger than the short-run effect, indicating the negative cumulative effect of capital flight on investment over time (Effiom et al. 2020: 358).

Fisseha, F.L. 2022. Effect of capital flight on domestic investment: Evidence from Africa

Fisseha (2022) carried out a study testing the association between capital flight and domestic investment in African countries. The author used data for 30 African countries from the period of 2000 to 2019.

Data on capital flight was measured by applying the methodology created by Ndikumana and Boyce (2021), which conceptualises capital flight as the difference between total capital inflows and recorded foreign exchange outflows. Domestic investment measured by total gross fixed capital formation scaled by GDP while controlling for other determinants of investment. The study also considered the effect of financial liberalisation – measured using an index on of countries’ capital account openness – on domestic investment.

The author models the relationship between capital flight and domestic investment using the dynamic generalised method of moments (GMM) approach, which he states is able to ‘correct for unobserved country heterogeneity omitted variable biases, measurement error, and endogeneity problems’ (Fisseha 2022: 11).

The results indicate that capital flight negatively and significantly affects total domestic investment, even after controlling for macroeconomic variables such as gross domestic saving, credit to the private sector, term of trade and trade openness. Fisseha (2022: 16) calculates that for each dollar that leaves a country in the form of capital flight, the economy is deprived of between 8 and 13 cents of domestic investment. Interestingly, the impact of financial liberalisation was found to be insignificant. However, the author acknowledges he was unable to account for the effect of financial liberalisation on capital flight itself.

Kasongo, A. 2022. The Impact of Capital Flight on Domestic Investment: Empirical Evidence from South Africa.

Kasonogo (2022) investigates the effect of capital flight on domestic investment in South Africa. The author relies on data for the period 1980-2018. Kasonogo uses Ndikumana and Boyce’s (2019) methodology on trade misinvoicing to serve as a measure for capital flight. Domestic investment is proxied using data from the World Bank’s World Development Indicators on gross capital formation as a percentage of GDP.

Kasongo ran regressions using an auto regressive distributed lag (ARDL) method that enables the capturing of both short and long-term effects. She found the effect was statistically significant and that in the short run, a 10% increase in capital flight resulted in a 0.5 % decrease in investment. In the long run, a 10% increase in capital flight was calculated to lead to a 2.5% decrease in domestic investment (Kasongo 2022: 10). This led Kasongo (2022: 1) to conclude ‘a persistent outflow of capital has a negative cumulative effect on domestic investment over time’.

Lawal, A.I., et al. 2017.Capital flight and the economic growth: Evidence from Nigeria, Binus Business Review, 8(2), 125-132.

Lawal et al (2017) investigate the impact of capital flight and its determinants on economic growth in Nigeria. Data for the period from 1981 to 2015 was taken from the Central Bank of Nigeria Statistical Bulletin for the dependent variable (GDP) and independent variables including foreign direct investment, foreign reserve, current account balance and external debt. Capital flight was estimated using the residual approach developed by the World Bank (1985).

The authors use the auto regressive distributed lag (ARDL) model to analyse the data. Their results indicate that capital flight had a negative long-run impact on economic growth in Nigeria during the period studied.

Madrueno, R. and Silberberger, M. 2023. Illicit financial flows and the growth of developing countries: Unravelling the intricacies of a growing global problem.

This paper attempts to estimate the effects of illicit financial outflows on economic growth in developing countries. To do so, Madrueno and Silberberger use a panel dataset from 2000 to 2013 on IFFs from Global Financial Integrity, which includes estimates of both trade misinvoicing and ‘hot money’. However, the authors reduce the GFI estimates by 50% to account for potential overestimation of IFFs due to methodological assumptions made by GFI (as explained above on page 11) (Madrueno and Silberberger 2023: 18-20).

The study relies on a regression in which illicit financial outflows act as the independent variable and gross national income (GNI) per capita growth acts as the dependent variable. Madrueno and Silberberger (2023) control for a range of factors such as institutional quality and socio-political conditions that may affect growth.

The paper finds that illicit outflows have a significant negative direct relationship with economic growth (Madrueno and Silberger 2023: 5). Specifically, a 10% increase in the volume of IFFs is correlated with a 1.5 % reduction in the biannual (rate of growth of GNI per capita) (Madrueno and Silberberger 2023: 21). Over the 7 two-year periods assessed, GNI per capita growth rate was found to be 11% lower for each 10% increase in the volume of illicit outflows (Madrueno and Silberberger 2023: 21). Given that, according to GFI data, illicit outflows increased by an estimated 220% in the same 14-year period, this suggests that the effect of illicit outflows in restricting growth in per capita GNI was significant.

This effect is not equal for all countries; Madrueno and Silberberger (2023: 26) find that countries with better governance, including strong regulatory frameworks and corruption controls, are less affected by the negative effects of IFF outflows. On the other hand, IFFs tend to have a more damaging effect on economic growth in countries in which tax revenue is lower than 30% of GDP (Madrueno and Silberberger 2023: 26). Moreover, in countries with higher levels of trade and foreign direct investment as a share of GDP, illicit outflows generate greater negative impacts on GNI per capita growth (Madrueno and Silberberger 2023: 26). The authors note that given that trade misinvoicing comprises the majority of illicit flows in GFI estimates, this is not surprising.

Maloney, M., Somerville, T. and Unger, B. 2019. Combatting money laundering in BC real estate. Province of British Columbia

This is a study by an expert panel on money laundering, commissioned by the Ministry of Finance of Canada. Maloney et al. (2019) assess how money laundering works in real estate markets, specifically the effect of money laundering on real estate prices.

The study employs several steps to analyse the impact of money laundering. First, to estimate the scale of money laundering in Canada and British Columbia, Maloney et al. (2019: 45) adopted and refined the gravity model first developed by Walker (1999). While acknowledging the large margin of error of estimates of the volume of money laundering, the authors use crime statistics reported to the United Nations, combined with assumptions about the proportion of the proceeds of crime that are laundered (as opposed to used directly by criminals). They then use a gravity model to calculate how laundered funds flow between countries, resulting in an estimate that the volume of money laundering in Canada in 2015 was approximately CAD$41 billion.

Next, Maloney et al. (2019: 87) analysed this in conjunction with data provided by the Canadian financial intelligence unit (FINTRAC) on the number of suspicious transaction reports relating to the real estate sector. Based on this information, the authors (2019: 2) estimate that approximately 5% of real estate transaction values are attributable to the effects of money laundering. As such, they conclude that money laundering causes distortions and inflations in the real estate market in Canada, artificially inflating house prices by somewhere in the region of 3.7 to 7.5% (Maloney et al. 2019: 57).

Real estateinvestments motivated by the desire to launder money constitute a significant resource misallocation because they are not driven by commercial or social purposes. The impact of money laundering in raising house prices also has secondary effects on the economy, as the extra money that home buyers spend on houses is not being spent or invested in other more productive assets or sectors that have multiplier effects (Maloney et al. 2019: 14).

Mevel, S., Ofa, S.V. and Karingi, S. 2013. Quantifying illicit financial flows from Africa through trade mispricing and assessing their incidence on African economies.

Mevel et al. (2013) assessed the effect of estimated illicit financial flows, proxied by data on trade mispricing, on African economies. Their estimate of trade misinvoicing builds on the IMF’s DOTS-based trade mispricing model, meaning they compared bilateral data to determine if there were residuals that reflected under-invoiced exports and over-invoiced imports.

However, some adjustments were made to the methodology, including the use of the UN COMTRADE dataset to provide more granular data than that provided by the IMF DOTS dataset. While the IMF DOTS trade mispricing model only uses information at the country level, UN COMTRADE provides bilateral trade information on 5,000 products, allowing for sectoral analysis. The authors also decided to use import data provided by BACI, because they state that: i) the BACI dataset uses a variance analysis to assess the reliability of country reporting on trade; and ii) it incorporates robust econometric analysis of the estimated transport costs that could partly explain residual differences in price between export and import prices (Mevel et al. 2013: 11).

The authors then employ a multi-country and multi-sector dynamic model, employing the modelling international relationships in applied general equilibrium (MIRAGE) approach. In this way, they estimate that, between 2001 and 2010, Africa lost US$409 billion due to trade mispricing, 92.5% of which constituted export under-invoicing with the remainder accounted for by import over-invoicing.

Interestingly, Mevel et al. (2013) found that the bulk of these losses were concentrated in a few countries and sectors. Egypt, Morocco, Nigeria and the member countries of the Southern African Customs Union were particularly affected, and the largest losses occurred in resource extraction sectors, especially crude and refined oil, metals and minerals.

Mpenya, H. et al. 2015. The effects of capital flight from oil and wood sectors on economic growth in Cameroon

This paper investigates the relationship between capital flight from trade misinvoicing in the oil and timber sectors and its impact on economic growth in Cameroon.

First, the authors attempt to quantify capital flight attributable to trade misinvoicing in these sectors. To do so, they apply the ‘sources-and-uses’ method of identifying discrepancies in balance of payment statistics between Cameroon and industrialised countries, drawing on reported trade data compiled by the United Nations (COMTRADE) and the World Bank (World Integrated Trade Solution). Using the same datasets, the authors then compare commercial transactions between Cameroon and its six largest industrialised trading partners in the oil and timber sectors to calculate the total volume of misinvoicing in those industries. This was calculated to be nearly US$8.9 billion in the period between 1995 and 2012 (Mpenya et al. 2015: 14).

Finally, after estimating the sector-specific losses due to trade misinvoicing in the sector, Mpenya et al. (2015) simulate a scenario in which these lost funds were productively reinvested in the economy, in order to estimate potential GDP growth lost to capital flight in the oil and timber sectors. Here, the authors rely on data on GDP and fixed capital formation provided by the IMF and the National Institute of Statistics of Cameroon. Using the incremental capital output ratio (ICOR) – which represents the amount of capital required to obtain an additional unit increase of production output – they estimate that if funds lost to capital flight had been reinvested in Cameroon, annual GDP growth could have increased with 0.21% additionally between 1995 and 2001, about 0.54% in the period 2002-2012.

Narea, A. 2018 The impact of illicit financial flows on economic growth of Ethiopia. A time series empirical analysis, 2000-2015. Quaderni DEM, 7

This study analyses the impact of IFFs on economic growth in Ethiopia in the period 2000-2015. First, to estimate the scale of illicit outflows in Ethiopia, the author adopts the same approach as Global Financial Integrity, by combining hot money narrow estimates with an analysis of trade misinvoicing.

For the estimates of hot money, Narea (2018) thus uses balance of payment statistics from the National Bank of Ethiopia, while to estimate trade misinvoicing affecting Ethiopia, the author relies on Direction of Trade Statistics provided by the IMF. Combining the estimated volume of hot money (an average of around US$242.5 million per year and US$3.8 billion in total) with the estimated amount lost to trade misinvoicing (calculated to be US$2.1 billion annually on average and US$33 billion for the whole period), the author estimates Ethiopia lost a total of US$37 billion dollars in illicit outflows between 2000 and 2015. It is worth noting that the data from the National Bank of Ethiopia appears rather patchy; Narea (2018: 20) is only able to estimate the volume of hot money for six years in the period from 2000 to 2015.

After estimating the scale of illicit outflows, Narea (2018) attempts to gauge their impact on GDP growth in Ethiopia, drawing on macroeconomic data from the Ministry of Finance and Development, the National Bank of Ethiopia and the World Bank. The author then employs various statistical tests, such as the augmented Dickey-Fuller and cointegration tests, to check whether the relationship between the illicit outflows and GDP remains stable over time. Ultimately, Narea (2018: 14) concludes that illicit outflows have a long-term negative effect on Ethiopia’s economic growth: a 1% increase in IFFs leads to a 2.79% decrease in the rate of GDP growth.

Ndiaye, A.S. 2014. Capital flight from the Franc zone: Exploring the impact on economic growth. Research Paper No. 269. African Economic Research Consortium.

Ndiaye’s (2014) study aims to analyse the impact of capital flight on economic growth between 1970 and 2010 in the Franc Zone, that is the African countries that use the CFA franc as a currency. In the zone, there is a fixed exchange rate between the CFA franc and the Euro as well as the free circulation of capital, which the authors argue contributes to capital flight from the region.

Ndiaye (2014) draws on two World Bank datasets (Global Development Finance and World Development Indicators), as well as two IMF datasets (Balance of Payment Statistics and Direction of Trade Statistics). He uses these to measure capital outflows by adopting the World Bank (1985) residual method, adjusted for exchange rate fluctuations, trade misinvoicing and inflation – as recommended by Boyce and Ndikumana (2001).

Using this data, the author estimated that capital flight for these countries equated to US$86.8 billion between 1970 and 2010, which was five times higher than the level of domestic investment in the same period. Ndiaye (2014) also found that, for the economies studied, whenever capital flight increased, the rate of economic growth decreased, and vice versa.

However, the author recognises that capital flight can be endogenous in economic growth models (as expectations of slow growth might affect the level of capital flight) (Ndiaye 2014: 21). There the author adopted the generalised method of moments (GMM) model to correct for endogeneity problems. The results demonstrated that capital flight had a statistically significant causal negative effect on economic growth in the region.

Ndiaye (2014: 21) also found that capital outflows had a statistically significant effect on investment, levels of credit to the private sector and domestic savings, and on the quality of institutions.

Ndikumana, L. 2014. Capital flight and tax havens: Impact on investment and growth in Africa. De Boeck Université 22, 99-124.

This paper investigates how capital flight (defined as ‘the net unrecorded capital flows between a country and the rest of the world’) and the use of tax havens affect domestic investment – an important determinant of economic growth – in Africa. The author conducts econometric analysis of panel data from 39 countries from 1970 to 2010.

Capital flight estimates for those countries are taken from two previous studies by the same author (Boyce and Ndikumana 2012; Ndikumana and Boyce 2011). These studies adopted the standard balance of payment ‘residual method’ (also known as the sources-and-uses method) to observe differences between recorded inflows and outflows of foreign exchange to provide a baseline ‘residual’ measure of capital flight. While the primary source of this data was the IMF’s Balance of Payment Statistics, the authors complemented this with data on debt flows from the World Bank’s Global Development Finance database to account for the fact that – according to them (Ndikumana and Boyce 2012: 4) – external borrowing was often underreported in the IMF’s Balance of Payment Statistics.

Having established baseline figures for the residual estimate of capital flight, the authors then augmented this with estimates of the scale of trade misinvoicing and unrecorded worker remittances, using data from the IMF’s Direction of Trade Statistics database and the International Fund for Agricultural Development, respectively.

Combining estimates for the two different groups of countries covered in Boyce and Ndikumana (2012a) and (2012b), Ndikumana (2014: 100) calculates that the total capital flight for the 39 countries between 1970 and 2010 equated to US$1.3 trillion.

In the 2014 study, Ndikumana outlines two main channels through which capital flight could negatively affect domestic investment: i) the depletion of domestic savings (both private and public) that reduces domestic capital formation; and ii) the creation of macroeconomic uncertainty, which discourages both private and public investment.

Ndikumana (2014: 103) investigates the impact of capital flight on total gross fixed capital formation and private investment as a percentage of GDP. Domestic bank credit to the private sector, gross domestic savings, and the volume and terms of trade are control variables (Ndikumana 2014: 109-112). Data on GDP and is taken from the World Bank’s World Development Indicators.

The regression results demonstrate that capital flight has a statistically significant and sizeable negative impact on both total domestic investment and private investment. The paper then simulates what the 39 countries’ GDP growth rates could have been if funds lost to capital flight had instead been invested domestically. To do so, Ndikumana (2014: 114) takes the same approach as Mpenya et al. (2015), by using the incremental capital output ratio (ICOR) method. These simulations suggest that had the funds lost to capital flight been reinvested domestically, on average across the 39 countries studies, the annual GDP growth rate between 1970 and 2010 would have been 2.4% higher (Ndikumana 2014: 118).

Overall, the author argues that this demonstrates the opportunity costs for African economies represented by capital flight, given its effect in reducing the amount of capital available domestically for productive investment by both public and private actors and, by extension, constraining economic growth (Ndikumana 2014: 120).

Nyathi, L. and Mutale, J. 2024. An ARDL approach to evaluating illicit financial flows & economic development in Zimbabwe. International Journal of Research and Scientific Innovation.

This study purports to examine the effect of IFFs on GDP in Zimbabwe between 2000 and 2023. However, the authors select as their independent variable the Corruption Perceptions Index (CPI) as a proxy for IFFs, which drastically undermines the validity of their findings for two main reasons. First, as a perception-based measure of the level of corruption in the public sector, the CPI has little relevance to the concept of transnational illicit financial flows. Second, the CPI scores before 2012 were not comparable.

The data for the dependent variable, GDP, is taken from the World Bank, and although the CPI is produced by Transparency International, the authors mistakenly state their source for Zimbabwe’s CPI scores is likewise the World Bank.

Nyathi and Mutale (2024) use econometric modelling (an auto regressive distributed lag regression model) to analyse the impact of changes in FDI, domestic savings or CPI scores between 2000-2023 on economic growth. The coefficient between one year’s CPI score and the following year’s GDP growth is calculated to be -1.66, indicating that CPI scores may have a negative impact on economic growth. However, the coefficients between CPI score and GDP growth in the same year as well as between CPI score and GDP growth two years later are positive (Nyathi and Mutale 2024: 230), suggesting the findings are random and unreliable. This may be due to the fact that annual CPI scores were not comparable before 2012. Moreover, CPI scores are not a good measure of the impact of illicit flows on economic growth, and the study contains elements of plagiarism of a previous study by Chirowamhangu (2023) as well as several factual errors, which further undermines confidence in the reported results.

Novaro, R., Piacenza, M. and Turati, G. 2022. Does money laundering inflate residential house prices? Evidence from the Italian provincial markets. Kyklos, 75(4), pp. 672–691.

This study investigates how money laundering affects residential house market prices in Italy, thereby shedding some light on how illicit financial flows impact advanced economies. However, it is important to note that the authors do not distinguish between the effects of domestic and transnational money laundering on house prices. Indeed, given the proxy for the volume of money laundering they select (see below), it is likely that the vast majority of the effect they document is the result of the laundering of the proceeds of crime committed within Italy by organised criminal groups. As such, this study can only provide limited insight on the effects of transnational IFFs.

To test the relationship between money laundering and house prices, the authors construct a novel dataset on residential house prices at the provincial level between 2005 and 2012, based on data provided by the Italian Ministry of Economy and Finance. They develop a proxy of the volume of criminal proceeds in a given province, namely the number of detected crimes related to drug dealing, trade in stolen goods and prostitution. Various market and non-market control variables are included (GDP per capita in each province, unemployment rate, age profile, percentage of university students, interest rate on deposits, waste disposal, public transport and so on) (Novaro et al. 2022: 677).

Overall, the study finds that money laundering inflates residential house prices significantly in provinces characterised predominantly by entrepreneurial forms of organised crime. They suggest this is because organised crime gangs purchase residential properties in these provinces as a means of laundering the proceeds of crime, increasing demand for housing stock (Novaro et al. 2022: 688). Conversely, in provinces marked by violent crime, criminal activity depresses house prices as people are reluctant to move to those areas.

Ogbonnaya, A.K. and Ogechuckwu, O.S. 2017. Impact of illicit financial flow on economic growth and development: Evidence from Nigeria. International Journal of Innovation and Economic Development. vol 3 (4). pp19-33.

The authors set out to appraise the impact of IFFs on economic growth in Nigeria between 1980 and 2015. The authors use Global Financial Integrity’s data on IFFs, though it is unclear whether they assess illicit inflows, outflows or both. For GDP data, they rely on data provided by the Central Bank of Nigeria.

The variables of IFFs and economic growth were subject to augmented Dickey-Fuller and cointegration tests, which revealed them to have a stable, long-term relationship. Ogbonnaya and Ogechuckwu (2017: 27) state that the adjusted R-squared of 56% indicates that more than half of the variance in GDP growth in Nigeria is explained by illicit financial flows. However, the potential causal mechanisms behind this relationship are not explored in the study.

Padil, H., Kasim, E., Razali, F., Atan, R., and Aminullah, H. 2022. Effect of quality of governance on the relationship between illicit financial flows and economic growth. Journal of Financial Crime, 29(4), 1382.

This study investigates the effect of i) IFFs and ii) quality of governance on economic growth, focusing on nine ASEAN countries: Thailand, Indonesia, Singapore, Malaysia, Brunei Darussalam, Cambodia, Lao People’s Democratic Republic, Myanmar, Vietnam and the Philippines.

In terms of the independent variables, the authors rely on the six indicators provided by the Worldwide Governance Indicators (WGI) for the quality of governance, while for IFFs they use the estimates provided for the nine countries under consideration by Global Financial Integrity. It is unclear whether the authors assess illicit inflows, outflows or both. The dependent variable, GDP per capita, is measured using data for 2008 to 2017 from the World Development Indicators, while control variables such as population, consumption, labour and capital are likewise drawn from the World Development Indicators (Padil et al. 2022: 1388).

Padil et al. (2022) use these data sources to run regressions (adopting partial least squares structural equation modelling) to test three hypotheses: (i) IFF negatively affect economic growth; (ii) quality of governance positively affects economic growth; and (iii) quality of governance moderates the negative impact of IFF on economic growth.

Padil et al. (2022: 1390) find that IFFs, in isolation from quality of governance, have a statistically significant negative impact on economic growth, corresponding to a coefficient of -0.152. They also find that higher quality of governance limits the negative impact of illicit flows on economic growth (Padil et al. 2022: 1391), implying that IFFs have a particularly destructive impact on growth in countries with low quality institutions.

Salandy, M. and Henry, L. 2013. The impact of capital flight on investment and growth in Trinidad and Tobago, 1971–2008.

Salandy and Henry (2013) empirically studied the impact of capital flight from Trinidad and Tobago on growth and investment between 1971 and 2008. They used the residual model of capital flight, adjusted for trade misinvoicing and inflation. Data on domestic investment and GDP was drawn from the Central Statistical Office of Trinidad and Tobago.

The authors used two estimation techniques for their econometric analysis: vector error correction model(VECM) for the short run and long-run analysis and the generalised method of moments (GMM) to corroborate the analysis.

The authors found an inverse relationship between capital flight and domestic investment. The VEC model resulted in a finding that an increase in capital flight of one dollar results in investment falling by $0.46 in the long run and $0.3 in the short run, holding all other factors constant (Salandy and Henry 2013: 8). The GMM estimation, employed to address potential problems of endogeneity, found smaller but still significant effects; all things being equal, a one dollar increase in capital flight in the previous year reduces the level of domestic investment by $0.17 the following year. Finally, the authors estimated that a one dollar increase in capital flight reduces real GDP by 0.02%.